Hello, and welcome to my little corner of the world (wide web). My name is Deb Evans, and I am a creative multipreneur in NW Houston successfully running multiple businesses and a few side gigs, because, why not? When I was a child, I rejected the idea that I had to choose just one thing to “be” when I grew up! On this page, you will learn about what I do and how to find out more if you’d like to connect. To learn more about me, check out my About Me Page.

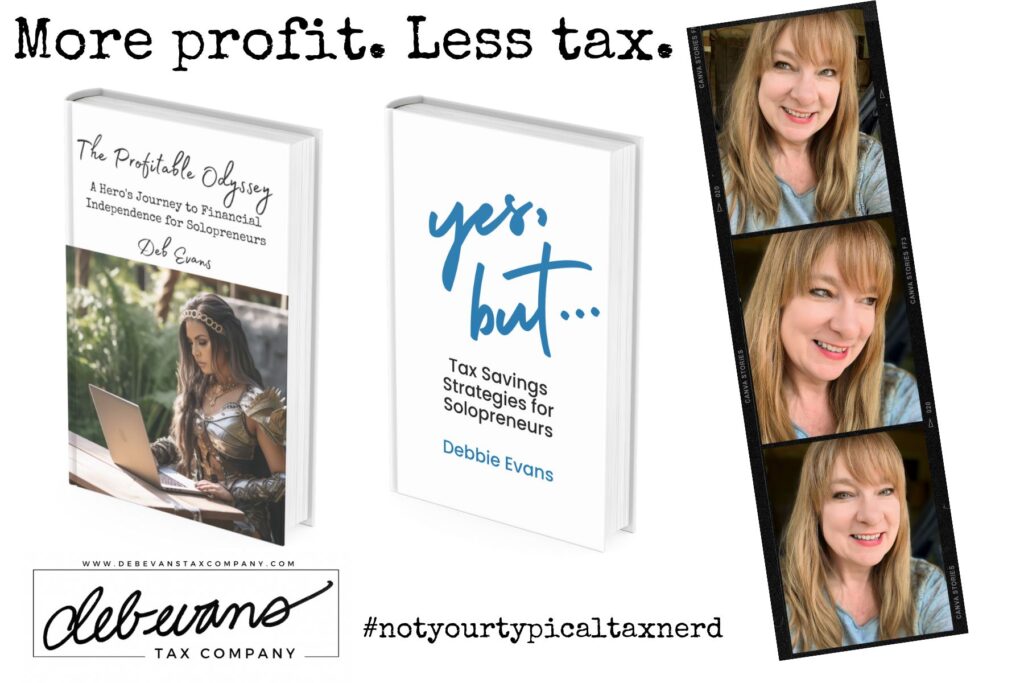

I’m a Tax Strategist and a Financial Coach, specializing in helping Solopreneurs increase PROFITS while reducing TAXES! But, I hate math. So, definitely not your typical tax nerd… still a nerd – just more of a Word Nerd, the kind that loves to stay up all night reading, writing, and watching movies like Star Wars, The Princess Bride, and Harry Potter.

I’m an Enrolled Agent, which is a federally licensed tax professional. The IRS recognizes EAs in the same category as CPAs and Tax Attorneys when it comes to tax work. At its core, being a tax pro is more about words than numbers – shocking, right? I spend 30-50 hours each year learning tax law and how to apply it to my clients’ needs. I extensively study tax planning strategies to help my clients keep as much of their hard-earned profits out of the government’s hands as is legally and ethically possible. I still know my way around a Profit & Loss Statement and can advise you on your numbers, but what I am best at is helping you use those numbers to grow your business.

As a Financial Coach, I love to work on Mindset issues and help you uncover Money Blocks that create your own Glass Ceiling. I have written two books in this area – The Profitable Odyssey and Taming Your Money Dragon, plus my flagship book Yes, But… Tax Savings Strategies for Solopreneurs. My real world experience as a successful business owner for three decades outside of my tax bubble helps me to better relate to my clients’ overall needs. I get it because I’ve done it, and I’m still doing it! To learn more about my work as a Tax Strategist and Financial Coach, please visit my website at www.debevanstaxcompany.com My books are available on Amazon, as well as through my website.

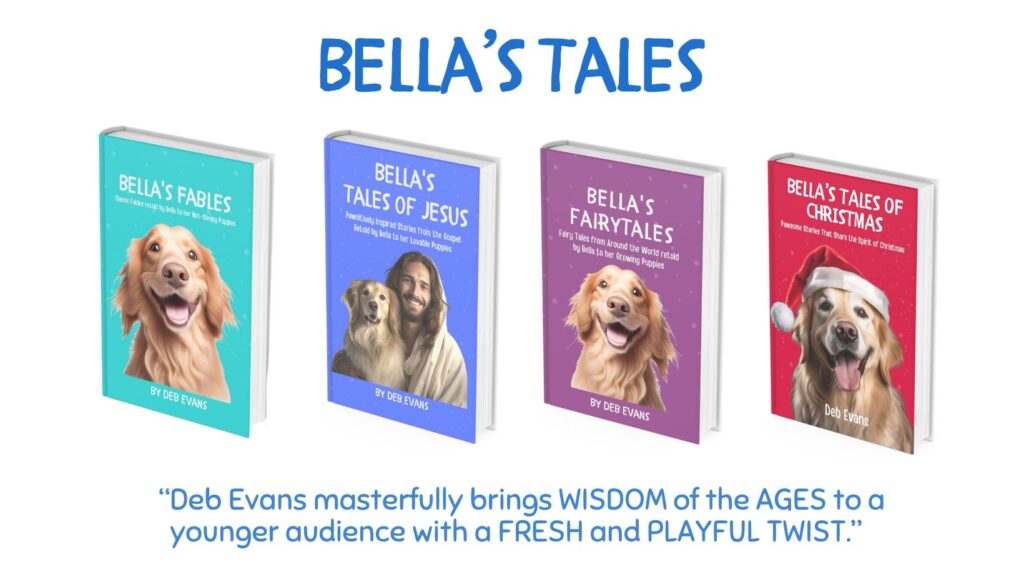

I have written and published five children’s books, four from my Bella’s Tales series. This is my newest venture, and it is truly a passion project. Bella is a Golden Retriever mother of three very active puppies who do not want to settle down at bedtime. Bella learns that sharing stories with her pups helps them settle down at night, but also gives the family much cherished family time together. In the first book, Bella’s Fables, Bella shares classic fables with the puppies. Bella’s Fairytales presents lesser known fairytales from around the world. Bella’s Tales of Jesus teaches the stories of the Gospel, and Bella’s Tales of Christmas features legends and stories such as The Christmas Star, the Christmas Tree, and St. Nicholas, as well as original stories, including the puppies’ own Christmas Miracle. I also wrote The Vowel Puppies, an introduction to reading, and I will be expanding it to a reading curriculum in 2024. To follow my writing adventures, visit www.debevansauthor.com

I am a private tutor teaching struggling and dyslexic children, K-3rd grade, to read! Using the latest Science of Reading methods, combined with a genuine love for reading and for helping children discover – if not a love for reading – an interest in reading, I have been teaching young children as a private instructor for over 20 years. I have specialized in teaching struggling and dyslexic readers for over ten of those years, and I have taken extensive training on the latest Science of Reading methods, including Orton Gillingham (a buzzword in dyslexia circles). My teaching approach combines this research-based approach with my natural enthusiasm for reading and teaching to create my own unique and engaging style of teaching.

To learn more about my tutoring business, visit www.debevanstutor.com .

Thank you for visiting! I hope we find a way that we can work together.